The JobKeeper wage subsidy scheme is being extended into March 2021.

Before you jump for joy too much, there’s a few changes that you will need to be across.

Key JobKeeper changes

- Introduction of two tiers of payments

- Employees with history of working 20hours per week will get one rate and other eligible employees will receive a lower rate

- The tiers will reduce from current JobKeeper 1.0 rates

- The tiers will reduce again for the second extension period from 4th January

The below infographic shows the changes in tiers

- Need to re-test eligibility based on actual turnover

- Unlike original JobKeeper where you could estimate income reductions, the extension periods will require you to test eligibility on ‘actual’ income

- You also cannot choose the accounting method that you use to calculate the ‘actuals’ instead you will need to use the same reporting method that you use for your GST reporting – that is cash or accruals. If you’re not sure which one you use check your last BAS as it is noted on this

- You need to qualify for each extension period

- Extension 1 from 28 September to 3 January: Use September 2020 quarterly actuals

- Extension 2 from 4 January to 28 March: Use December 2020 quarterly actuals

- Alternative tests exist again for re-testing eligibility for each extension period. You can find more details of these here.

- In addition to satisfying the eligibility test for the extension period you also must satisfy the original decline in turnover test

- For the Extension 1 period this is simple to do as by satisfying the extension period you also satisfy the original turnover test.

- For businesses that were claiming JobKeeper 1.0 (even based on projected income) you have also satisfied the original turnover test

- The ‘tricky’ bit will be businesses that do not sustain a downturn until the December 2020 quarter that didn’t satisfy the original decline in turnover test nor the September 2020 quarter test. These businesses will likely be locked out of JobKeeper 2.0 even if their business has a significant downturn in the December 2020 quarter.

Seems simple enough?? Not too fast, there’s a few more things you’re going to have to do.

Steps you need to take

Firstly, you’re going to be comparing your actuals to the same period last year – with the ATO matching the reporting method to your BAS they are also going to be data-matching against your prior lodged BAS. If you have outstanding BAS lodgements, for whatever reason, you need to get these up to date quickly as well as ensure that your 2020 lodgements are taken care of promptly.

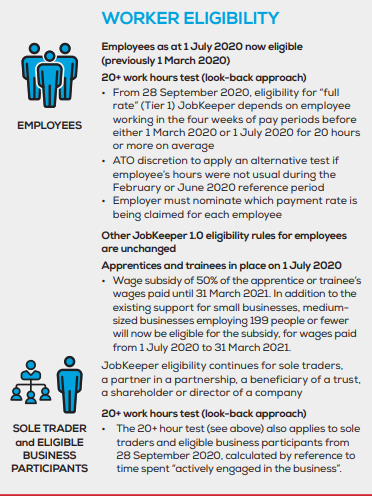

You’re also going to have to assess what tier your employees fall under:

- Eligible employees have been extended to include test date of both 1 March 2020 AND 1 July 2020

-

- If you previously had casuals that didn’t meet the ‘long term casual’ definition – they may now be eligible by testing at 1 July 2020

- You will need to assess work hours to work out what tier an employee should be on (This is done via a ‘look back’ approach)

-

- You will be testing the number of hours worked in a 28 day period

- You will include additional hours for worked overtime, paid leave and paid public holidays

- The 28 day period will be the pay period that ended just before to 1 March or 1 July

- You can test employees for both periods and then select the period that gives the best result / highest tier

- To qualify for the highest tier you need to get to 80 hours within the 28 day period for the employee

- You will be testing the number of hours worked in a 28 day period

For Eligible Business Participants we are still awaiting guidance from the ATO on how you can demonstrate the hours that you were ‘actively engaged’ in your business during the test periods.

OK – so you’ve assessed your business and your employees eligibility – how do you get your money?

If you were enrolled in JobKeeper 1.0

- If you are already receiving JobKeeper payments, you don’t need to enrol again

- You will need to check that you meet the ongoing eligibility requirements

- You will need to inform the ATO what tiers your eligible employees qualify for – check with your software provider on how to do this

- You also need to notify your employees what tier they qualify for within 7 days of notifying the ATO

- You will need to ensure that you meet the wage conditions for fortnights ending in October by 31st October

- You’ll need to submit monthly declarations to claim between the 1st and 14th of the following month (same as you have been doing for JobKeeper 1.0)

If you’re new to JobKeeper

- You can enrol with the ATO using Business Portal or through your Tax or BAS Agent (note whoever enrols becomes responsible for the monthly declaration and reporting)

- Check you meet the eligibility requirements

- Identify eligible employees and get them to complete nomination form stating that they aren’t receiving jobkeeper from another employer

- Identify the tier that each employee qualifies for and notify both the ATO and the employee

- Ensure you meet the wage conditions

- Submit your monthly declaration between 1st and 14th of following month to ATO to claim subsidy

Finally – don’t forget to document all your calculations and decisions in the event that you’re selected for an ATO review. Also with the introduction of two tiers communication with staff as to which tier they qualify for will be very important. Finally, with the reduction in jobkeeper rates and the government’s objective to eventually wean employers off support you will also need to start considering your staffing requirements, overheads and costs into the future.

More information

ATO dedicated JobKeeper resources